What’s in the name?

-William Shakespeare.

Well, if you are in modern India, earning individual who wishes to save your hard earned savings in some institution licensed by Government, just to keep your OWN money with them, you need a name..!!

Not a new name for you, but a name for your proposed account to be opened, which is corroborated by third party, usually Government agency through some document confirming your identity and stating your basic details.

Indeed, this is KYC…….!!!

KYC is a process of establishing customer information by a financial institution involving:

Identification >>>>> Confirmation>>>>> Verification>>>>> Declaration

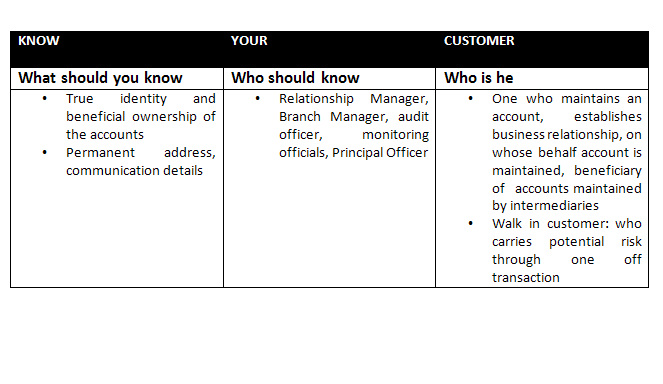

KYC explained:

Therefore in simple language your KYC is your banking passport which enables you as a customer for “ON BOARDING” a banking relationship.

Some years before while I was undergoing articleship in CA firm under able guidance of very senior Chartered Accountant, we had this monthly concurrent audit of nationalized bank. It was my first month and when I looked at the report format it started with Deposits, new accounts opened during the month and KYC compliance thereof. As instructed by boss was checking the account opening forms and I asked him, why do we check this? He explained in simple language that KYC was like establishing DNA, purporting your identity confirmation so that your whereabouts are established. So like DNA establishes your biological record, KYC does of your identity and enables to carry out banking relationship.

This requirement of KYC is not left to Banking alone, various other financial intermediaries governed by regulatory agencies like IRDA, SEBI would require Insurance Companies and Stock market intermediaries to conduct KYC.

Dissection of KYC

-William Shakespeare.

Well, if you are in modern India, earning individual who wishes to save your hard earned savings in some institution licensed by Government, just to keep your OWN money with them, you need a name..!!

Not a new name for you, but a name for your proposed account to be opened, which is corroborated by third party, usually Government agency through some document confirming your identity and stating your basic details.

Indeed, this is KYC…….!!!

KYC is a process of establishing customer information by a financial institution involving:

Identification >>>>> Confirmation>>>>> Verification>>>>> Declaration

KYC explained:

Therefore in simple language your KYC is your banking passport which enables you as a customer for “ON BOARDING” a banking relationship.

Some years before while I was undergoing articleship in CA firm under able guidance of very senior Chartered Accountant, we had this monthly concurrent audit of nationalized bank. It was my first month and when I looked at the report format it started with Deposits, new accounts opened during the month and KYC compliance thereof. As instructed by boss was checking the account opening forms and I asked him, why do we check this? He explained in simple language that KYC was like establishing DNA, purporting your identity confirmation so that your whereabouts are established. So like DNA establishes your biological record, KYC does of your identity and enables to carry out banking relationship.

This requirement of KYC is not left to Banking alone, various other financial intermediaries governed by regulatory agencies like IRDA, SEBI would require Insurance Companies and Stock market intermediaries to conduct KYC.

Dissection of KYC

But wait, KYC is not just this, it is:

• Making reasonable efforts to determine the true identity and beneficial ownership of accounts;

• Identifying sources of funds

• Verifying nature of customers’ business

• And analyzing what constitutes reasonable account activity?

As advised by RBI, this is NOT KYC

• Denial of Service to the Common Person: w.r.t “ Small accounts”

• Intrusive Behavior from banking staff

• Use of information for cross selling of banking or third party products

• Harassment of customers- threatening to close down the accounts arbitrarily, reporting suspicious activity, publishing information causing public embarrassment or any acts that would endanger customer-banker relationship.

Why KYC norms for banks?

The answer is why security checks at places of importance, sensitive zones, VIP offices?

To verify, whether the person is allowed (authorized) to enter, he will not pose threat/harm/injury to premises/ its reputation.

Similarly, in banking KYC is required to understand who you are, where you have come from, what is your purpose of banking and how will you carry this relationship?

Sound KYC procedures have particular relevance to the safety and soundness of banks, in that:

a. They help to protect banks’ reputation and the integrity of banking systems by reducing the likelihood of banks becoming a vehicle for or a victim of financial crime and suffering consequential reputational damage;

KYC: INDIAN APPROACH FROM BANKING REGULATOR RBI

As India’s Central Bank, RBI purpose of KYC is to safeguard banks from being used by criminal elements for money laundering activities and to enable banks to understand the risk posed (through customers, products and services, delivery channels). The purpose of the above regulation will entail banks to assess internally and prudently manage its risk.

However, is fully aware KYC framework should not be intrusive in nature nor too strict resulting in denial of banking services to general public. Even the recent Government initiatives of PMJDY (Pradhan Mantri Jan Dhan Yojana) have encouraged banking for all but with adequate safeguards.

A lot of people always crib that, KYC is just a decade or so old and since its inception has been a trouble for them to carry their routine banking activities.

Interestingly, that is not so. KYC word was coined in the decade of 2000’s but the origins have been half a century old in India. Amazingly, I was aware of it while studying a subject called “Banking Laws” recently introduced in Professional: Final stage of Company Secretary Examinations, while preparing to teach the same.

Brief history of KYC in India:

Decade wise analysis:

1. 1960-1970: RBI asked banks to ensure full and correct addresses of all depositors were recorded. This was with an intention to avoid Benami transactions. (Benami transactions are those which are carried out in names of fictitious persons). Although the act came much later, so surprising that today it has gained significance. Yes, the AADHAAR, UCIN number drawn on benami avoiding concept so that subsidies rolled out do not reach middlemen and fictitious beneficiaries are eliminated.

2. 1970-1980: concept of “Introduction” made applicable. In order to avoid benami transactions and an independent third party acknowledgement of acquaintance, introducer was introduced. Infact, as I read in the IIBF material for KYC/AML; the Negotiable Instruments Act of 1881 u/s 131 has provided legal protection to bankers.

3. 1980-1990: The reasonable gap of 6 months when introducer opens his account and introduces someone else defined.

4. 1990-2000: Some significant guidelines

* Cash transactions monitoring: Basically as a measure to avoid diversion of funds by withdrawal of cash from CC/Overdraft accounts.

* Practice of obtaining photographs of all operative account holders w.e.f 1st January, 1994.

* No cash transaction above INR 50,000/- for TC’s/DD/MT/TT.

The first KYC circular was launched in 2002. The detailed guidelines with operative procedures started from 2004.

In one of my interaction with RBI IO: Inspecting Officer during audit I hesitatingly asked, the KYC guidelines refined since 2004, prior to that how was banking being done without KYC? Being born in late 1980’s and since attainting age of majority and mind of maturity, the banking I have seen is with KYC and indeed with computerized operations. (I really appreciate the older version of bankers who carried the ardent task of banking MANUALLY).

>>>>>His answer was politically correct, he politely said KYC procedures were carried out by bankers according to their internal instructions, since there were no concrete guidelines; it was own discretion of bankers, without knowing it is KYC. Fair enough.

The shift in awareness levels and bringing out such detailed guidelines was due to enactment of Prevention of Money Laundering Act, 2002 and FIU IND being set up in 2004-05.

The four pillars of KYC:

1. Customer Acceptance Policy

2. Customer Identification Procedures

3. Risk profiling

4. Monitoring of transactions

*Staff training and awareness to customers also an integral part of it.

Detailed information of what they are, RBI website has beautifully narrated it.

Refer http://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=9074

KYC ASSIMILATION FLOW

(Note: This is recommendatory; some steps would be added or skipped, modified or changed with higher level approvals. The process flow will change according type of customer, business he carries and also associated with form of organization, other aspects as decided). In any case, KYC would not be compromised, the customer would not be put to undue hardships, yet the guidelines RBI expects banks to comply will be followed in spirit, not necessarily in letter.

1. Giving account opening form along with Customer Id form (UCIN) to customer after explaining what is to be done with guidelines. Pre-numbered account opening forms advisable.

2. Filling mandatory columns by the customer in legible ink usually in Capital letters preferred

3. Affixing recent colour photograph of customer after verifying his face in person.

4. Specimen signature card, rather the box to be signed by the customer in presence of bank officials

5. Instructions on mode of operation of accounts to be ticked, whether single/joint/power of attorney.

6. Cheque book facility/Debit Card if preferred would be ticked.

7. Nomination to be written as per (not compulsory, but always advisable). If the customer is specific about nomination confirmation, the nomination registered on his account can be acknowledged via letter, usually passbook or statement of account will depict it.

8. Presenting photocopies of Original KYC: Identity and Address proof and correspondingly verifying the same with original documents. Any additional documents, i.e more than one address or ID proof is always welcome.

9. After verifying the same, the bank official has to authorize: sign and give noting, if required.

10. Depending on type of customer and additional information obtained by personal inquiry from him in areas like, purpose of account opening, source of income, mode of credits expected: cash or otherwise, business/profession carried out by him, specific geographical details if warranted, “Risk profile” to be decided, marked and if circumstances warrant, due diligence on enhanced grounds would be carried out by higher level officials.

11. The form would be processed and field would be checked and correctly entered in the system. EDD if warranted would be carried out. The system would generate and code the customer chronologically, a series of numbers that would act as basis of all accounts attached to this code, termed as Customer Id or as RBI calls it, Unique Customer Identification Code*

12. After the code is noted on the form, it would be authorized by a higher officials after due verification, effectively two persons have verified the form, concept of “4 EYES”. The specific type of account requested would be opened. Introduction is not compulsory.

13. The account once opened, the welcome kit: passbook of the customer with add-ons, if required like cheque book, debit card would be issued to customer after noting and acknowledgement of receipt from him. A welcome hand shake follows.

14. At the back end, if required EDD would be undertaken, even in case of simple due diligence if warranted, details of his identity documents like PAN card would be checked in the GoI NSDL database, passport no would be verified. For address proof, a personal visit by staff followed with a visit report thereof would be done.

15. Ideally, a “Letter of Thanks” would be dispatched to the address mentioned on the form, to verify the genuineness of address. A telephonic call welcoming the customer would be value addition welcoming him in your banking family, seeking his requirement details and accordingly rolling out products for him, pure banking starts.

List of acceptable documents for KYC

They are called OVD: Officially Valid Documents. This is a standard indicative checklist. The link is directly given by RBI. Any one document as Identity proof and another for address proof would be sufficient. Usually, bankers would ask for more than one. Although RBI says, the aadhar card can be both an identity as well as address proof, I would still go for one document, since profile creation would be helpful.

The link for OVD is

http://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=9074

WHAT HAPPENS AFTER KYC IS COMPLETE?

After KYC is done, that is Customer Id: account opening form and presenting documents, there would be no further ask from customer. The customer will not be approached unless the bank deems necessary or while periodic updation of KYC.

After your KYC is done, the profile of customer would be created. Risk profile as it is called, basically is a scorecard of associated risks you carry for the relationship with the banker. This scorecard will determine;

· Level of due diligence required

· Monitoring of transactions

· Assessing the activities in the accounts

· Seeking additional information when deemed necessary.

· Reporting obligation fulfillment on the account qualifying for the same

· Periodic (semi-annual) risk profile upgradation

Don’t worry..!!!

Your risk profile is not CIBIL. Banker will not share this with any other financial institution, agency or even with legal heirs. It will be only documented for banks risk management purposes and if necessary, being a mandatory field reported to only statutory authorities.

WHY CUSTOMER ID FORM WHEN THE ACCOUNT OPENING FORM IS ALREADY THERE?

Valid question, the answer is Customer Id as popularly called or UCIN form is core crux of KYC. The account opening, i.e savings, current or term deposit is a banking product. So your KYC is attached with Customer Id. The account bears your details, instructions and a medium of carrying out your transactions since UCIN is just a code, not an account.

The purpose of Customer ID is:

WILL MY KYC DETAILS & DOCUMENTS WITH THE BANK REMAIN CONFIDENTIAL?

YES, Yes, yes…!!! Definitely, under banker-customer relationship, the bank will not disclose any of your identity: address or account related details to anyone, unless there is legally a binding to do so.

The BCSBI: Banking Codes and Standards Board of India under “Code of Commitment to Customers”, Clause 5 “Privacy and Confidentiality” specifically states, the personal information of customer shall be private and confidential, even when you are no longer a customer.

Your information will never be revealed to anyone, neither to outsiders nor to the group of institutions affiliated to banking. The exceptions would be only when, customer permits in writing for revealing information, duty towards public or as required under law. Even when other bankers reference is needed, written permission from the customer would be sought. So chill, you might inadvertently reveal information, the banker never will.

After all; the banker is not just a custodian of your funds, but a custodian of your faith and your valuable/sensitive information.

WHAT IF MY KYC IS ALREADY DONE IN ANOTHER BANK, DO I NEED KYC WHILE I OPEN AN ACCOUNT IN NEW BANK?

Unfortunately, yes. Every bank will do ensure their own KYC. The reason is simple, no bank wants to take a chance relying on some other banks KYC, and after all relying on their KYC the risk is not shared. Besides, every bank would have internal system of their own KYC and would want every new customer to pass through their checks and system.

This problem would be solved once we have a national data portal of individuals. With aadhar the process was initiated, but looks distant dream at the moment.

Fortunately though, you would not require KYC for opening/transferring account from one branch of same bank to another branch of the same bank. RBI has permitted and actually reprimanded bankers for not following “Intra Bank KYC portability”.

The other aspects of KYC like what documents to present when, address proof and identity proof different or other smaller aspects is already given by RBI beautifully summarized on their website. I will be trying to draw attention to matters which are not reported, probable questions from a Banker’s point of view:

WHILE KYC IS COMPLETE IN ALL ASPECTS, CAN I STILL INSIST ON KYC UPDATION EVERY YEAR?

No, RBI has given guidelines on this issue. The guidelines on periodic KYC updation are on the basis of risk profile. Therefore greater the risk perceived by the banker, frequency of KYC updation would be more.

At present the RBI stipulates, time intervals for periodic updating of existing KYC for Low/ Medium/ High risk customers would be 10/8/2 years respectively.

CAN ANY CUSTOMER SUE THE BANKER UNDER CONSUMER LAWS OR OTHER LAWS FOR PARTIAL FREEZING OF ACCOUNT FOR NON FULLFILLMENT OF KYC?

Note: Partial freezing is simply debit freezing/disallowing withdrawals from account.

Ok. This is tricky. It is very hard to say since, the problem is peculiarly Indian. The regulator RBI permits partial freezing of accounts after due notice (3 months) for partial freezing of account, BUT Gujarat High Court has thrown a “Googly”.

In a decided case law with India’s biggest bank, a customer whose account had been frozen for non compliance of KYC formalities, the learned Court has opined, partial freezing which is allowing stray credits but freezing debits, seriously hampers the customer of utilizing his own money and puts him under risk of offence u/s 138 of Negotiable Instruments Act, 1881 for cheques being dishonored; is wrong. Therefore bank can be vindicated by Banking Ombudsman (sadly RBI’s own body) and customer given relief.

This landmark judgement though from 2012, for people like me in AML as well as Banking Ombudsman Scheme field, lands us in a precarious position. It no doubt serves the customer well, but again the same provisions given by RBI on partial freezing can be complained against in Ombudsman scheme which is RBI managed only.

Although facts of the case are very unique, the aggrieved customer being lodged in jail and could not come personally to present KYC documents had not been given sufficient time by the bank. He sought bail for the purposes of personal appearance in bank for submitting documents which was rejected. Writ petition filed by him, sought this order from court.

My practical advice is, partial freezing or full freezing, better to put more efforts in complying, i.e performing re-KYC as much as possible and keeping the “freezing” option as last resort.

The other practical way of avoiding legal liability is; newspaper advertisement for all customers in general in bilingual newspaper with highest circulation in the district, giving 3 months notice in writing to fulfill KYC else account would be freezed, followed by another final reminder giving another 30 days time and then proceed with partial freezing.

HOW KYC HELPED ME IN BANKING?

During my experience in banking filed, I was pre-dominantly working in compliances. Two such incidents:

1. Deposits section: In one of our Mumbai branch, I encountered a potential customer wishing to open his account. On inquiry he was a second hand car dealer. His documents seemed to be perfectly in order. The only issue was his partner was not available to personal face-to-face meeting. His documents seemed correct. As they say, TGTBT (To Good to be true). We promised him of visit to his showroom only after that account would be processed. On verification, the other partners PAN card was found to be fake, the PAN number had a different name, on verifying residential details of both the partners, the electricity bills submitted, for the customer no, and there was no record on the database. Next morning, during sudden visit we found his showroom to be almost empty, just a few cars, whereas we expected lot of used cars parked for sale. His answers were not satisfactory and on our condition of personal appearance of other partner he backed off. We filed STR under “Attempted Category”. Several months later, during a seminar somewhere other Co-op banker told us a story how his bank was duped in a fraud vehicle loan scheme where X customer encashed the DD given by the bank by depositing in account opened by car dealer who had approached us. Both customer X and dealer were gone. Several days we were called for inquiry by EOW since we filed STR for that customer.

Wish the other bank had not been so casual, fraud would have been averted. KYC, rescued our bank….!!!

2. Loan section: In X branch a lady from Y city approached us for small personal loan. She confessed she works in different city and her salary being deposited there she would offer us PDC’S, loan would be in her name as she was eligible and the loan amount was for her fathers small business. We accepted application and started scrutiny. We sent a casual letter to her employer confirming her identify and asking her Salary details as she had authorized us. We sent the letter along with her photograph. It worked, the employer replied they had such an employee, the name and other details were correct, however she was not the one as seen in photo sent by us. We were startled; the employer sought our permission in sending the right lady whose name those documents were to our branch. She met us and we lodged a complaint, on investigation it was found. The culprit was educated daughter of Xerox shop owner, who while taking photocopies of her records saved a copy of all her documents each. She thought banker would confirm at the maximum under name, we sent inquiry with photograph and we saved our institution of a possible fraud. Alas, the original lady was our happy customer later.

I would appreciate comments.

Thanks for the valuable time.

My intention of this blog was to clear the air to some people, who think KYC is Kick & Harass your customer.

No, KYC actually is KNIT-&-VALUE-YOUR CUSTOMER……!!!!

Credits: RBI Notifications, Press Releases, Deputy Governor’s speeches and Archives. Indian Institute of Banking and Finance Course material for examination in KYC/AML.

Amit Retharekar.

• Making reasonable efforts to determine the true identity and beneficial ownership of accounts;

• Identifying sources of funds

• Verifying nature of customers’ business

• And analyzing what constitutes reasonable account activity?

As advised by RBI, this is NOT KYC

• Denial of Service to the Common Person: w.r.t “ Small accounts”

• Intrusive Behavior from banking staff

• Use of information for cross selling of banking or third party products

• Harassment of customers- threatening to close down the accounts arbitrarily, reporting suspicious activity, publishing information causing public embarrassment or any acts that would endanger customer-banker relationship.

Why KYC norms for banks?

The answer is why security checks at places of importance, sensitive zones, VIP offices?

To verify, whether the person is allowed (authorized) to enter, he will not pose threat/harm/injury to premises/ its reputation.

Similarly, in banking KYC is required to understand who you are, where you have come from, what is your purpose of banking and how will you carry this relationship?

Sound KYC procedures have particular relevance to the safety and soundness of banks, in that:

a. They help to protect banks’ reputation and the integrity of banking systems by reducing the likelihood of banks becoming a vehicle for or a victim of financial crime and suffering consequential reputational damage;

- They provide an essential part of sound risk management system (basis for identifying, limiting and controlling risk exposures in assets & liabilities)

- They serve an important national objective of preventing an act or terror, whether external enemy or internal rebellion by prompt reporting.

KYC: INDIAN APPROACH FROM BANKING REGULATOR RBI

As India’s Central Bank, RBI purpose of KYC is to safeguard banks from being used by criminal elements for money laundering activities and to enable banks to understand the risk posed (through customers, products and services, delivery channels). The purpose of the above regulation will entail banks to assess internally and prudently manage its risk.

However, is fully aware KYC framework should not be intrusive in nature nor too strict resulting in denial of banking services to general public. Even the recent Government initiatives of PMJDY (Pradhan Mantri Jan Dhan Yojana) have encouraged banking for all but with adequate safeguards.

A lot of people always crib that, KYC is just a decade or so old and since its inception has been a trouble for them to carry their routine banking activities.

Interestingly, that is not so. KYC word was coined in the decade of 2000’s but the origins have been half a century old in India. Amazingly, I was aware of it while studying a subject called “Banking Laws” recently introduced in Professional: Final stage of Company Secretary Examinations, while preparing to teach the same.

Brief history of KYC in India:

Decade wise analysis:

1. 1960-1970: RBI asked banks to ensure full and correct addresses of all depositors were recorded. This was with an intention to avoid Benami transactions. (Benami transactions are those which are carried out in names of fictitious persons). Although the act came much later, so surprising that today it has gained significance. Yes, the AADHAAR, UCIN number drawn on benami avoiding concept so that subsidies rolled out do not reach middlemen and fictitious beneficiaries are eliminated.

2. 1970-1980: concept of “Introduction” made applicable. In order to avoid benami transactions and an independent third party acknowledgement of acquaintance, introducer was introduced. Infact, as I read in the IIBF material for KYC/AML; the Negotiable Instruments Act of 1881 u/s 131 has provided legal protection to bankers.

3. 1980-1990: The reasonable gap of 6 months when introducer opens his account and introduces someone else defined.

4. 1990-2000: Some significant guidelines

* Cash transactions monitoring: Basically as a measure to avoid diversion of funds by withdrawal of cash from CC/Overdraft accounts.

* Practice of obtaining photographs of all operative account holders w.e.f 1st January, 1994.

* No cash transaction above INR 50,000/- for TC’s/DD/MT/TT.

The first KYC circular was launched in 2002. The detailed guidelines with operative procedures started from 2004.

In one of my interaction with RBI IO: Inspecting Officer during audit I hesitatingly asked, the KYC guidelines refined since 2004, prior to that how was banking being done without KYC? Being born in late 1980’s and since attainting age of majority and mind of maturity, the banking I have seen is with KYC and indeed with computerized operations. (I really appreciate the older version of bankers who carried the ardent task of banking MANUALLY).

>>>>>His answer was politically correct, he politely said KYC procedures were carried out by bankers according to their internal instructions, since there were no concrete guidelines; it was own discretion of bankers, without knowing it is KYC. Fair enough.

The shift in awareness levels and bringing out such detailed guidelines was due to enactment of Prevention of Money Laundering Act, 2002 and FIU IND being set up in 2004-05.

The four pillars of KYC:

1. Customer Acceptance Policy

2. Customer Identification Procedures

3. Risk profiling

4. Monitoring of transactions

*Staff training and awareness to customers also an integral part of it.

Detailed information of what they are, RBI website has beautifully narrated it.

Refer http://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=9074

KYC ASSIMILATION FLOW

(Note: This is recommendatory; some steps would be added or skipped, modified or changed with higher level approvals. The process flow will change according type of customer, business he carries and also associated with form of organization, other aspects as decided). In any case, KYC would not be compromised, the customer would not be put to undue hardships, yet the guidelines RBI expects banks to comply will be followed in spirit, not necessarily in letter.

1. Giving account opening form along with Customer Id form (UCIN) to customer after explaining what is to be done with guidelines. Pre-numbered account opening forms advisable.

2. Filling mandatory columns by the customer in legible ink usually in Capital letters preferred

3. Affixing recent colour photograph of customer after verifying his face in person.

4. Specimen signature card, rather the box to be signed by the customer in presence of bank officials

5. Instructions on mode of operation of accounts to be ticked, whether single/joint/power of attorney.

6. Cheque book facility/Debit Card if preferred would be ticked.

7. Nomination to be written as per (not compulsory, but always advisable). If the customer is specific about nomination confirmation, the nomination registered on his account can be acknowledged via letter, usually passbook or statement of account will depict it.

8. Presenting photocopies of Original KYC: Identity and Address proof and correspondingly verifying the same with original documents. Any additional documents, i.e more than one address or ID proof is always welcome.

9. After verifying the same, the bank official has to authorize: sign and give noting, if required.

10. Depending on type of customer and additional information obtained by personal inquiry from him in areas like, purpose of account opening, source of income, mode of credits expected: cash or otherwise, business/profession carried out by him, specific geographical details if warranted, “Risk profile” to be decided, marked and if circumstances warrant, due diligence on enhanced grounds would be carried out by higher level officials.

11. The form would be processed and field would be checked and correctly entered in the system. EDD if warranted would be carried out. The system would generate and code the customer chronologically, a series of numbers that would act as basis of all accounts attached to this code, termed as Customer Id or as RBI calls it, Unique Customer Identification Code*

12. After the code is noted on the form, it would be authorized by a higher officials after due verification, effectively two persons have verified the form, concept of “4 EYES”. The specific type of account requested would be opened. Introduction is not compulsory.

13. The account once opened, the welcome kit: passbook of the customer with add-ons, if required like cheque book, debit card would be issued to customer after noting and acknowledgement of receipt from him. A welcome hand shake follows.

14. At the back end, if required EDD would be undertaken, even in case of simple due diligence if warranted, details of his identity documents like PAN card would be checked in the GoI NSDL database, passport no would be verified. For address proof, a personal visit by staff followed with a visit report thereof would be done.

15. Ideally, a “Letter of Thanks” would be dispatched to the address mentioned on the form, to verify the genuineness of address. A telephonic call welcoming the customer would be value addition welcoming him in your banking family, seeking his requirement details and accordingly rolling out products for him, pure banking starts.

List of acceptable documents for KYC

They are called OVD: Officially Valid Documents. This is a standard indicative checklist. The link is directly given by RBI. Any one document as Identity proof and another for address proof would be sufficient. Usually, bankers would ask for more than one. Although RBI says, the aadhar card can be both an identity as well as address proof, I would still go for one document, since profile creation would be helpful.

The link for OVD is

http://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=9074

WHAT HAPPENS AFTER KYC IS COMPLETE?

After KYC is done, that is Customer Id: account opening form and presenting documents, there would be no further ask from customer. The customer will not be approached unless the bank deems necessary or while periodic updation of KYC.

After your KYC is done, the profile of customer would be created. Risk profile as it is called, basically is a scorecard of associated risks you carry for the relationship with the banker. This scorecard will determine;

· Level of due diligence required

· Monitoring of transactions

· Assessing the activities in the accounts

· Seeking additional information when deemed necessary.

· Reporting obligation fulfillment on the account qualifying for the same

· Periodic (semi-annual) risk profile upgradation

Don’t worry..!!!

Your risk profile is not CIBIL. Banker will not share this with any other financial institution, agency or even with legal heirs. It will be only documented for banks risk management purposes and if necessary, being a mandatory field reported to only statutory authorities.

WHY CUSTOMER ID FORM WHEN THE ACCOUNT OPENING FORM IS ALREADY THERE?

Valid question, the answer is Customer Id as popularly called or UCIN form is core crux of KYC. The account opening, i.e savings, current or term deposit is a banking product. So your KYC is attached with Customer Id. The account bears your details, instructions and a medium of carrying out your transactions since UCIN is just a code, not an account.

The purpose of Customer ID is:

- Single code will entail details of all your accounts with the bank. Deposits or otherwise. Single point synopsis would be available to the banker in deciding term deposit products to be offered on your request or deciding credit worthiness while adjudging loan request.

- The basic id is actually TDS. Yes…!! Many smart minds have tried to open accounts by different names citing purposes or otherwise to ensure the interest income on single account does not exceed INR 10,000/- after which TDS, tax will be deducted (withheld portion of interest) u/s 194A, Income Tax Act, 1961 and remitted to GoI directly. The document pertaining that credit, Form 16A would be given to you, in TRACES today for you to claim credit or seek refund from Income Tax Dept. Therefore, with a single uniform code, all deposit products under various schemes with varying amounts would be clubbed for applicability/ deduction purposes.

- Another hidden intention as I see it is NPA classification norms. Under these norms of a bad loan, sub-standard asset; the rules are borrower-wise and not facility wise. In simple words, if your personal loan of a smaller amount is overdue and turns NPA, because the norms are borrower wise, under a single Customer Id all your other loans would be visible, therefore all the loan accounts would be classified bad; i.e sub-standard. Quite a masterstroke from RBI….!!!

- The other angle may be, under the Customer ID, even balances lying in deposit accounts are visible and extractable, they could be used by banks simply to keep as margin against loan availed by those customers, which would lower risk weighted assets and hike CAR (Capital Adequacy Ratio).

WILL MY KYC DETAILS & DOCUMENTS WITH THE BANK REMAIN CONFIDENTIAL?

YES, Yes, yes…!!! Definitely, under banker-customer relationship, the bank will not disclose any of your identity: address or account related details to anyone, unless there is legally a binding to do so.

The BCSBI: Banking Codes and Standards Board of India under “Code of Commitment to Customers”, Clause 5 “Privacy and Confidentiality” specifically states, the personal information of customer shall be private and confidential, even when you are no longer a customer.

Your information will never be revealed to anyone, neither to outsiders nor to the group of institutions affiliated to banking. The exceptions would be only when, customer permits in writing for revealing information, duty towards public or as required under law. Even when other bankers reference is needed, written permission from the customer would be sought. So chill, you might inadvertently reveal information, the banker never will.

After all; the banker is not just a custodian of your funds, but a custodian of your faith and your valuable/sensitive information.

WHAT IF MY KYC IS ALREADY DONE IN ANOTHER BANK, DO I NEED KYC WHILE I OPEN AN ACCOUNT IN NEW BANK?

Unfortunately, yes. Every bank will do ensure their own KYC. The reason is simple, no bank wants to take a chance relying on some other banks KYC, and after all relying on their KYC the risk is not shared. Besides, every bank would have internal system of their own KYC and would want every new customer to pass through their checks and system.

This problem would be solved once we have a national data portal of individuals. With aadhar the process was initiated, but looks distant dream at the moment.

Fortunately though, you would not require KYC for opening/transferring account from one branch of same bank to another branch of the same bank. RBI has permitted and actually reprimanded bankers for not following “Intra Bank KYC portability”.

The other aspects of KYC like what documents to present when, address proof and identity proof different or other smaller aspects is already given by RBI beautifully summarized on their website. I will be trying to draw attention to matters which are not reported, probable questions from a Banker’s point of view:

WHILE KYC IS COMPLETE IN ALL ASPECTS, CAN I STILL INSIST ON KYC UPDATION EVERY YEAR?

No, RBI has given guidelines on this issue. The guidelines on periodic KYC updation are on the basis of risk profile. Therefore greater the risk perceived by the banker, frequency of KYC updation would be more.

At present the RBI stipulates, time intervals for periodic updating of existing KYC for Low/ Medium/ High risk customers would be 10/8/2 years respectively.

CAN ANY CUSTOMER SUE THE BANKER UNDER CONSUMER LAWS OR OTHER LAWS FOR PARTIAL FREEZING OF ACCOUNT FOR NON FULLFILLMENT OF KYC?

Note: Partial freezing is simply debit freezing/disallowing withdrawals from account.

Ok. This is tricky. It is very hard to say since, the problem is peculiarly Indian. The regulator RBI permits partial freezing of accounts after due notice (3 months) for partial freezing of account, BUT Gujarat High Court has thrown a “Googly”.

In a decided case law with India’s biggest bank, a customer whose account had been frozen for non compliance of KYC formalities, the learned Court has opined, partial freezing which is allowing stray credits but freezing debits, seriously hampers the customer of utilizing his own money and puts him under risk of offence u/s 138 of Negotiable Instruments Act, 1881 for cheques being dishonored; is wrong. Therefore bank can be vindicated by Banking Ombudsman (sadly RBI’s own body) and customer given relief.

This landmark judgement though from 2012, for people like me in AML as well as Banking Ombudsman Scheme field, lands us in a precarious position. It no doubt serves the customer well, but again the same provisions given by RBI on partial freezing can be complained against in Ombudsman scheme which is RBI managed only.

Although facts of the case are very unique, the aggrieved customer being lodged in jail and could not come personally to present KYC documents had not been given sufficient time by the bank. He sought bail for the purposes of personal appearance in bank for submitting documents which was rejected. Writ petition filed by him, sought this order from court.

My practical advice is, partial freezing or full freezing, better to put more efforts in complying, i.e performing re-KYC as much as possible and keeping the “freezing” option as last resort.

The other practical way of avoiding legal liability is; newspaper advertisement for all customers in general in bilingual newspaper with highest circulation in the district, giving 3 months notice in writing to fulfill KYC else account would be freezed, followed by another final reminder giving another 30 days time and then proceed with partial freezing.

HOW KYC HELPED ME IN BANKING?

During my experience in banking filed, I was pre-dominantly working in compliances. Two such incidents:

1. Deposits section: In one of our Mumbai branch, I encountered a potential customer wishing to open his account. On inquiry he was a second hand car dealer. His documents seemed to be perfectly in order. The only issue was his partner was not available to personal face-to-face meeting. His documents seemed correct. As they say, TGTBT (To Good to be true). We promised him of visit to his showroom only after that account would be processed. On verification, the other partners PAN card was found to be fake, the PAN number had a different name, on verifying residential details of both the partners, the electricity bills submitted, for the customer no, and there was no record on the database. Next morning, during sudden visit we found his showroom to be almost empty, just a few cars, whereas we expected lot of used cars parked for sale. His answers were not satisfactory and on our condition of personal appearance of other partner he backed off. We filed STR under “Attempted Category”. Several months later, during a seminar somewhere other Co-op banker told us a story how his bank was duped in a fraud vehicle loan scheme where X customer encashed the DD given by the bank by depositing in account opened by car dealer who had approached us. Both customer X and dealer were gone. Several days we were called for inquiry by EOW since we filed STR for that customer.

Wish the other bank had not been so casual, fraud would have been averted. KYC, rescued our bank….!!!

2. Loan section: In X branch a lady from Y city approached us for small personal loan. She confessed she works in different city and her salary being deposited there she would offer us PDC’S, loan would be in her name as she was eligible and the loan amount was for her fathers small business. We accepted application and started scrutiny. We sent a casual letter to her employer confirming her identify and asking her Salary details as she had authorized us. We sent the letter along with her photograph. It worked, the employer replied they had such an employee, the name and other details were correct, however she was not the one as seen in photo sent by us. We were startled; the employer sought our permission in sending the right lady whose name those documents were to our branch. She met us and we lodged a complaint, on investigation it was found. The culprit was educated daughter of Xerox shop owner, who while taking photocopies of her records saved a copy of all her documents each. She thought banker would confirm at the maximum under name, we sent inquiry with photograph and we saved our institution of a possible fraud. Alas, the original lady was our happy customer later.

I would appreciate comments.

Thanks for the valuable time.

My intention of this blog was to clear the air to some people, who think KYC is Kick & Harass your customer.

No, KYC actually is KNIT-&-VALUE-YOUR CUSTOMER……!!!!

Credits: RBI Notifications, Press Releases, Deputy Governor’s speeches and Archives. Indian Institute of Banking and Finance Course material for examination in KYC/AML.

Amit Retharekar.

RSS Feed

RSS Feed