A little attempt to understand your banking rights, BCSBI the guardian angel

http://indiaforensic.com/certifications/author/amit_ret/

AN OVERVIEW OF MONEY LAUNDERING LEGISLATIONS IN INDIA

AML CTF Framework in India:

Money laundering is a global menace and no jurisdiction is left untouched by it. The problem of money-laundering is no longer restricted to the geo-political boundaries of any country. India is no exception to this. In the current context, India is a lucrative investment destination for many, however; tax transparency and tax uniformity coupled with IPR regulations as well as need for strong laws against money laundering are the most common apprehensions that one has with this jurisdiction.

We will try to shed light on the AML legal scenario of India.

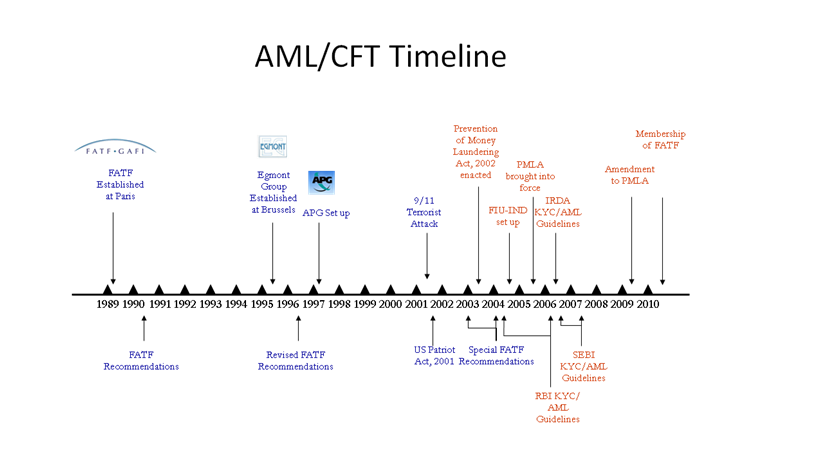

India has become a member of the Financial Action Task Force (FATF) and Asia Pacific Group on money-laundering, which are committed to the effective implementation and enforcement of internationally accepted standards against money-laundering and the financing of terrorism.

History:

In India, prevention of accumulation of illegal money and its confiscation is age old. It is only post 2000 that these laws were converged according to the global requirements.

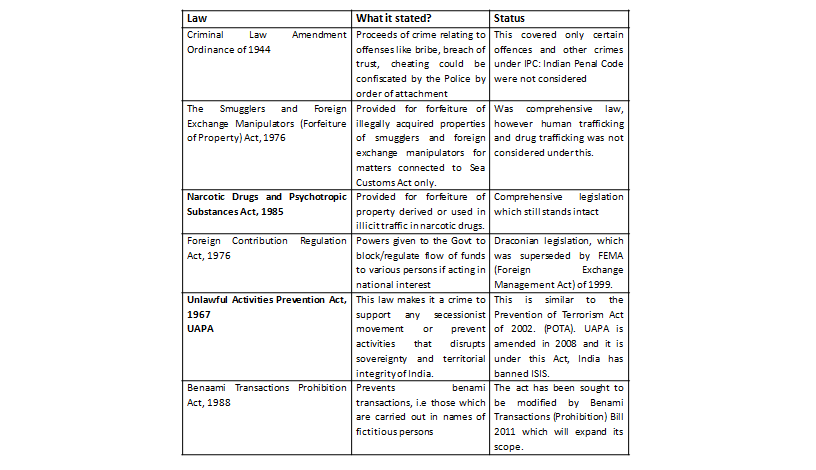

A brief snapshot of these legislations:

Money laundering is a global menace and no jurisdiction is left untouched by it. The problem of money-laundering is no longer restricted to the geo-political boundaries of any country. India is no exception to this. In the current context, India is a lucrative investment destination for many, however; tax transparency and tax uniformity coupled with IPR regulations as well as need for strong laws against money laundering are the most common apprehensions that one has with this jurisdiction.

We will try to shed light on the AML legal scenario of India.

India has become a member of the Financial Action Task Force (FATF) and Asia Pacific Group on money-laundering, which are committed to the effective implementation and enforcement of internationally accepted standards against money-laundering and the financing of terrorism.

History:

In India, prevention of accumulation of illegal money and its confiscation is age old. It is only post 2000 that these laws were converged according to the global requirements.

A brief snapshot of these legislations:

Prevention of Money Laundering Act, 2002 (PMLA)

This is a comprehensive legislation, encompassing all activities that could constitute money laundering.

PMLA is enacted adopting the political declaration and global programme of action of the resolution S-17.2 of 1990 and political declaration to adopt national money laundering legislation and programme in 1998 by the General Assembly of the United Nations.

This is a comprehensive legislation, encompassing all activities that could constitute money laundering.

PMLA is enacted adopting the political declaration and global programme of action of the resolution S-17.2 of 1990 and political declaration to adopt national money laundering legislation and programme in 1998 by the General Assembly of the United Nations.

PMLA Elaborated:

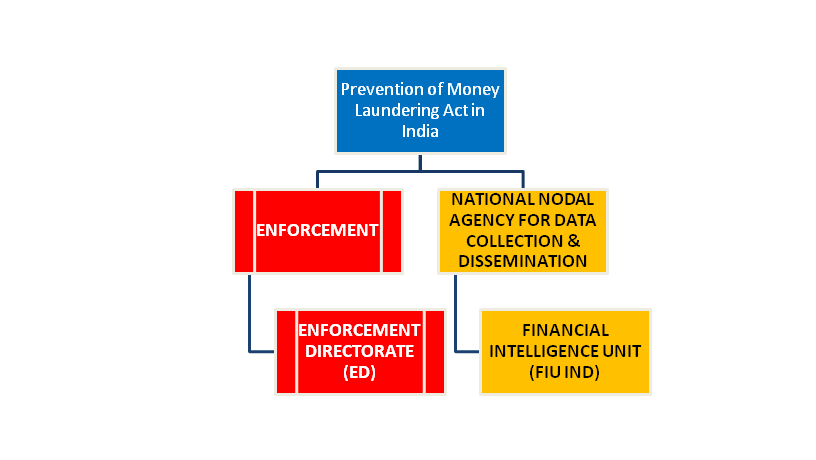

l Main Components

– Investigation of and prosecution for ML offences

l Enforcement Directorate: ED

– Obligations of the financial sector entities

l Financial Intelligence Unit-India: FIU IND

l Time Sheet

– Enacted on 17th Jan, 2003

– Brought into force from 1st July, 2005

– Amended in 2009 (w.e.f. 1st June 2009)

– Amended in 2012 (w.e.f 15th February 2013)

l Extention of this act : Applies to whole of India, including the state of Jammu & Kashmir (This is notable, since majority of Indian Laws don’t apply to this state)

The main objective of PMLA

l To Prevent, Combat and Control money laundering;

l To Confiscate and seize the property obtained from the laundered money;

l To deal with any other issue connected with money laundering in India.

ADMINISTRATION OF PMLA

l Main Components

– Investigation of and prosecution for ML offences

l Enforcement Directorate: ED

– Obligations of the financial sector entities

l Financial Intelligence Unit-India: FIU IND

l Time Sheet

– Enacted on 17th Jan, 2003

– Brought into force from 1st July, 2005

– Amended in 2009 (w.e.f. 1st June 2009)

– Amended in 2012 (w.e.f 15th February 2013)

l Extention of this act : Applies to whole of India, including the state of Jammu & Kashmir (This is notable, since majority of Indian Laws don’t apply to this state)

The main objective of PMLA

l To Prevent, Combat and Control money laundering;

l To Confiscate and seize the property obtained from the laundered money;

l To deal with any other issue connected with money laundering in India.

ADMINISTRATION OF PMLA

(* Both ED and FIU IND are under Department of Revenue, Ministry of Finance, Govt of India)

Some important phrases defined by PMLA, i.e Indian law definitions

Section 3: Money Laundering:

Whosoever directly or indirectly attempts to indulge or knowingly assists or knowingly is a party or is actually involved in any process or activity connected with the proceeds of crime and projecting it as untainted property shall be guilty of offence of money laundering”

Section 2(1)(u): Proceeds of crime

Any property derived or obtained, directly or indirectly, by any person as a result of criminal activity relating to a scheduled offence or the value of any such property;

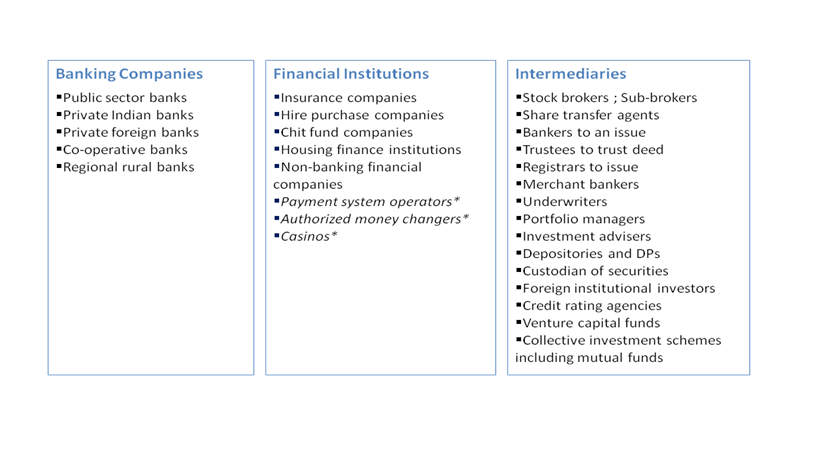

Obligations of REPORTING ENTITIES:

Under PMLA, following are the reporting entities:

Some important phrases defined by PMLA, i.e Indian law definitions

Section 3: Money Laundering:

Whosoever directly or indirectly attempts to indulge or knowingly assists or knowingly is a party or is actually involved in any process or activity connected with the proceeds of crime and projecting it as untainted property shall be guilty of offence of money laundering”

Section 2(1)(u): Proceeds of crime

Any property derived or obtained, directly or indirectly, by any person as a result of criminal activity relating to a scheduled offence or the value of any such property;

Obligations of REPORTING ENTITIES:

Under PMLA, following are the reporting entities:

Appointment of Principal Officer and Designated Director:

The rules under PMLA require, every RE to appoint a senior managerial person enumerated as “Principal Officer” who is given separate responsibility of AML activities and entrusted with the compliance thereof.

The Designated Director would be a person nominated from the Board of RE’s to oversee the compliance under this act.

It is pertinent to note that, these people have the sole responsibility of compliance under this act and are liable for criminal actions in case of default.

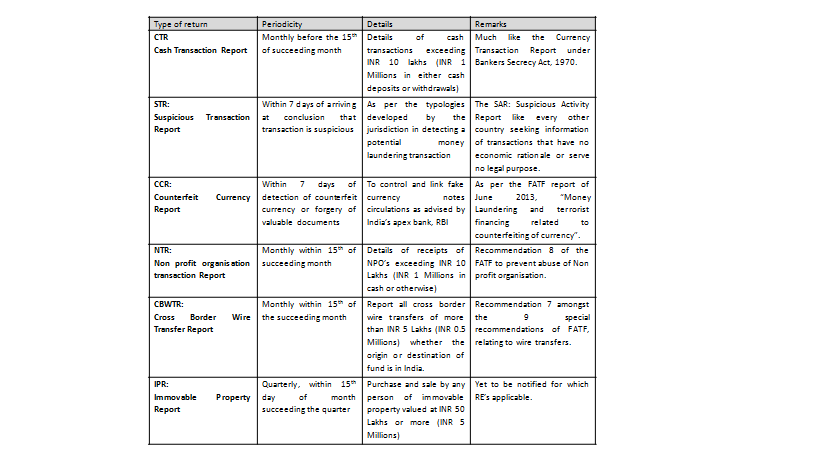

Furnishing of information:

Submission of information relevant for FIU IND by Indian entities called as RE’s (Reporting Entities is as under)

The rules under PMLA require, every RE to appoint a senior managerial person enumerated as “Principal Officer” who is given separate responsibility of AML activities and entrusted with the compliance thereof.

The Designated Director would be a person nominated from the Board of RE’s to oversee the compliance under this act.

It is pertinent to note that, these people have the sole responsibility of compliance under this act and are liable for criminal actions in case of default.

Furnishing of information:

Submission of information relevant for FIU IND by Indian entities called as RE’s (Reporting Entities is as under)

FINNET Gateway Portal:

The FIU IND introduced the FINNET gateway portal for online filing of mandatory returns by RE’s. This is an initiative of bringing a uniform structure of reporting under XML whereby all RE’s would be upload returns electronically using schema validation rules authenticated using DSC: Digital Signature of the Principal Officer.

It was released on test basis in August 2012 and online submission made mandatory since October 2012.

Link: https://finnet.gov.in

Effectiveness of FIU IND:

The FIU IND has been very keen on the RE’s with respect to submission of information for analysis and dissemination, the duality of control i.e:

· Banks being covered by their independent regulator; RBI: Reserve Bank of India

· Stock market intermediaries being enforced to their regulatory authority, SEBI: Securities & Exchange Board of India

· Insurance agencies under the ambit of IRDA, Insurance Development Authority of India

has somehow undermined the effectiveness of FIU IND. However, this has not prevented it from consolidation of information and timely disbursal to the agencies involved for sanctions/prosecutions of organisations/entities involved in heinous crime of money laundering.

Union Budget of India: 2015-16: GAME CHANGER

After the much anticipated change in guards in the Indian union government, their focus being bringing back the black money stashed abroad in tax havens, the constitution of SIT (Special Investigation Teams) has all played a major impact in creating an environment for effective AML regime in India.

Accordingly the Union of India has recognised, “tax evasion” as the 15th scheduled offence under the PMLA. Hence any act of tax evasion, i.e concealment of income or evasion of tax relation to foreign offense would be considered predicate offense. It means it would now amount to money laundering in the Indian context.

Other safeguards against money laundering:

1. Multi layered transactions and round tripping:

Multi-layering of transactions across countries including the round-tripping of unaccounted money generated from India, under section 58 A grants the power to the local court in India to decide matters on its merits, even when the person is acquitted by an overseas court.

This is especially for matters concerning black money.

2. Participatory Notes:

The huge uproar in the Indian Parliament that P-Notes (as they are popularly called are means of converting black money by sending money abroad and boom-e-ranging back without KYC), the amended law has asked SEBI (the securities market regulator) to set up a coordination mechanism in this regard with RBI so that funds flow into the domestic stock / securities markets is properly monitored.

3. Onus of proof between bonfide and malafide transaction:

Section 8 prescribes that onus of proof that the property in question is not out of proceeds of money-laundering crime, being not only on the accused but also on anyone who is in possession of the proceeds of crime, should be subject to adequate safeguards to protect the innocent.

4. Persons engaged in safe keeping and administration of cash and liquid securities on behalf of other persons

Tricky cases, wherein the IBA (Indian Bankers Association) submitted, it would be very difficult for banks to verify each transaction carried out by its clients, especially safe deposit lockers.

Therefore recommend that an appropriate declaration from the customer may be secured in the case of safe deposit lockers maintained by banks, so that the ordinary bank customer is not inconvenienced.

5. Audit

In the course of normal audit and inspection, the records of the banks can be mandated to be verified for their compliances under the anti-money laundering law as well. However wherever necessary, special audit would be carried out as per instructions of Director, FIU IND by Chartered Accountants India.

Some issue that India still needs to address:

1. Commodities market out of the ambit of PMLA

2. DNFBP sector not subjected to PMLA (except Casino):

The notified persons carrying on Designated Business or Profession are;

Department of Posts, Stock Exchanges, Entities registered with PFRDA (, entities who can be included when notified by the Government -Real estate agents, sub-registrars (registering immovable property authority ), dealers in precious metals/stones, high value goods and safe deposit keepers.

3. Effectiveness concerns due to absence of ML conviction

4. Identification and verification of beneficial ownership of legal persons

5. Ineffective sanctions regime for non-compliance.

6. Trade Based Money Laundering and issues thereto have yet not been addressed.

THE WAY FORWARD:

The regulators of each sector, RBI in case of banking etc, have been following up along with FIU IND for on-going compliance as well as improving the quality of reporting. Its just a beginning and the strides made India in this regard with a focused and concrete vision will surely pave way to install “culture” of compliance in institutions involved.

With the new crop of AML professionals emerging in India, there is bound to be progress in the areas of due diligence and reporting. Infact India has much to offer to the world in information sharing as well as best practises.

Amit Retharekar

The FIU IND introduced the FINNET gateway portal for online filing of mandatory returns by RE’s. This is an initiative of bringing a uniform structure of reporting under XML whereby all RE’s would be upload returns electronically using schema validation rules authenticated using DSC: Digital Signature of the Principal Officer.

It was released on test basis in August 2012 and online submission made mandatory since October 2012.

Link: https://finnet.gov.in

Effectiveness of FIU IND:

The FIU IND has been very keen on the RE’s with respect to submission of information for analysis and dissemination, the duality of control i.e:

· Banks being covered by their independent regulator; RBI: Reserve Bank of India

· Stock market intermediaries being enforced to their regulatory authority, SEBI: Securities & Exchange Board of India

· Insurance agencies under the ambit of IRDA, Insurance Development Authority of India

has somehow undermined the effectiveness of FIU IND. However, this has not prevented it from consolidation of information and timely disbursal to the agencies involved for sanctions/prosecutions of organisations/entities involved in heinous crime of money laundering.

Union Budget of India: 2015-16: GAME CHANGER

After the much anticipated change in guards in the Indian union government, their focus being bringing back the black money stashed abroad in tax havens, the constitution of SIT (Special Investigation Teams) has all played a major impact in creating an environment for effective AML regime in India.

Accordingly the Union of India has recognised, “tax evasion” as the 15th scheduled offence under the PMLA. Hence any act of tax evasion, i.e concealment of income or evasion of tax relation to foreign offense would be considered predicate offense. It means it would now amount to money laundering in the Indian context.

Other safeguards against money laundering:

1. Multi layered transactions and round tripping:

Multi-layering of transactions across countries including the round-tripping of unaccounted money generated from India, under section 58 A grants the power to the local court in India to decide matters on its merits, even when the person is acquitted by an overseas court.

This is especially for matters concerning black money.

2. Participatory Notes:

The huge uproar in the Indian Parliament that P-Notes (as they are popularly called are means of converting black money by sending money abroad and boom-e-ranging back without KYC), the amended law has asked SEBI (the securities market regulator) to set up a coordination mechanism in this regard with RBI so that funds flow into the domestic stock / securities markets is properly monitored.

3. Onus of proof between bonfide and malafide transaction:

Section 8 prescribes that onus of proof that the property in question is not out of proceeds of money-laundering crime, being not only on the accused but also on anyone who is in possession of the proceeds of crime, should be subject to adequate safeguards to protect the innocent.

4. Persons engaged in safe keeping and administration of cash and liquid securities on behalf of other persons

Tricky cases, wherein the IBA (Indian Bankers Association) submitted, it would be very difficult for banks to verify each transaction carried out by its clients, especially safe deposit lockers.

Therefore recommend that an appropriate declaration from the customer may be secured in the case of safe deposit lockers maintained by banks, so that the ordinary bank customer is not inconvenienced.

5. Audit

In the course of normal audit and inspection, the records of the banks can be mandated to be verified for their compliances under the anti-money laundering law as well. However wherever necessary, special audit would be carried out as per instructions of Director, FIU IND by Chartered Accountants India.

Some issue that India still needs to address:

1. Commodities market out of the ambit of PMLA

2. DNFBP sector not subjected to PMLA (except Casino):

The notified persons carrying on Designated Business or Profession are;

Department of Posts, Stock Exchanges, Entities registered with PFRDA (, entities who can be included when notified by the Government -Real estate agents, sub-registrars (registering immovable property authority ), dealers in precious metals/stones, high value goods and safe deposit keepers.

3. Effectiveness concerns due to absence of ML conviction

4. Identification and verification of beneficial ownership of legal persons

5. Ineffective sanctions regime for non-compliance.

6. Trade Based Money Laundering and issues thereto have yet not been addressed.

THE WAY FORWARD:

The regulators of each sector, RBI in case of banking etc, have been following up along with FIU IND for on-going compliance as well as improving the quality of reporting. Its just a beginning and the strides made India in this regard with a focused and concrete vision will surely pave way to install “culture” of compliance in institutions involved.

With the new crop of AML professionals emerging in India, there is bound to be progress in the areas of due diligence and reporting. Infact India has much to offer to the world in information sharing as well as best practises.

Amit Retharekar